The mystery of President Trump’s consulting fee income

President Trump’s continued ownership of his business empire while in office has raised a flood of ethical and security concerns that stem from his unprecedented blend of personal profiteering and public service. His near constant travel to and promotion of his businesses, along with large payments from special interests and foreign governments, have created thousands of conflicts of interest and undercut his claim that he has not been involved with the Trump Organization since becoming president.

Now, add to that unethical stew a new discovery: President Trump reported being paid consulting fees by the Trump Organization during his second year in office.

“The mere fact that a president might be engaged in for-profit consulting on the side is cause for concern.”

The mere fact that a president might be engaged in for-profit consulting on the side is cause for concern. The presidency is arguably the most demanding job in the world and requires anyone who holds it to have a single-minded focus on what’s in the best interests of the American people, not their personal financial interests. Beyond that, however, the fees raise new questions specific to Trump about how involved he is with his businesses and — in light of the recent New York Times reports about his tax returns — to what extent the payments might demonstrate his continued attempts to use questionable means to lower the Trump Organization’s tax burden.

Last year, Trump disclosed $61,045 in “consulting fees” that are apparently related to Trump Organization projects that never materialized in his financial disclosure report covering 2018. The payments are unusual because they are the only one of their kind that Trump has reported since becoming president. And unlike his more passive forms of profit from his businesses, the use of the term “consulting” seems to imply actual services rendered by the president.

Even if Trump did not provide consulting services in exchange for the fees, the question remains as to why the income was designated as consulting fees. It is impossible to draw a conclusion about that based on the financial disclosure alone, but the answer could lie in last month’s bombshell New York Times report which described the Trump Organization’s practice of writing off consulting fees as business expenses in order to reduce the Trump Organization’s tax burden.

Before he assumed office, Trump assured the public that he would not be involved with the Trump Organization’s operations while serving as president, despite maintaining an ownership interest in the company. While there is plenty of evidence that Trump has picked away at the so-called firewall between the presidency and the Trump Organization, it would be remarkable if, as the consulting fees suggest, Trump was paid for services he performed for the company while he was president.

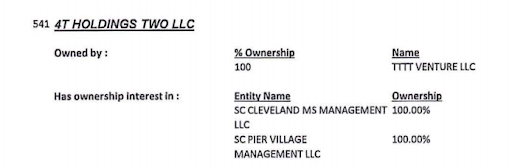

The financial disclosure, which covers 2018, is the only one he has filed since becoming president that reveals income from consulting fees. It was paid to him through an entity called 4T Holdings Two LLC. According to the disclosure, the LLC owns two entities, one of which appears to relate to a plan for the Trump Organization to build a development with Kushner Companies on the Jersey Shore that was scrapped in June 2018. The other is linked to a management deal between the Trump Organization and another hotel brand to develop a hotel in Mississippi. A note in the financial disclosure filed by Ivanka Trump affirms that connection. The Trump Organization abandoned its plans to develop the hotel, the first of its budget “Scion” line, in February 2019.

Ivanka Trump also has an interest in 4T Holdings Two LLC, but she arranged to receive fixed payments related to her interest in its parent company after she started working at the White House in order to avoid a situation in which her income would depend on the company’s performance. President Trump did not make a similar arrangement.

While there is only one reported payment for consulting fees in Trump’s financial disclosures, he also reported more than a dozen payments totalling millions of dollars for “management fees” in 2018 alone. It is unclear what distinguishes the consulting fees Trump reported from the management fees in his financial disclosures.

One possible explanation for the consulting fee payments is that the president provided consulting services to the Trump Organization while serving as president, contrary to his pledge to stay out of his company’s operations. But as last month’s New York Times article showed, there may be reasons to characterize payments as consulting fees even if Trump himself wasn’t a consultant.

While $61,045 is a small amount of money compared to the income Trump has generated from some of his other assets, designating the income as consulting fees may be part of a larger pattern to benefit the president financially. In its report, the Times describes how President Trump may have reduced his company’s tax burden by writing off $26 million in consulting fees as business expenses. The newspaper added that, in some of those cases, “people with direct knowledge of the projects were not aware of any outside consultants who would have been paid.”

The Times points specifically to the financial disclosure report that Ivanka Trump filed when she started working at the White House, which revealed that the income she received from a consulting company while she was also a Trump Organization employee “exactly matched consulting fees claimed as tax deductions by the Trump Organization for hotel projects in Vancouver and Hawaii.”

President Trump’s tax returns covering 2018, which might reveal whether the consulting fees Trump reported in his financial disclosure were part of an effort to reduce the Trump Organization’s tax burden, have not been made public. Until then, Trump’s consulting fee income remains a mystery.